As plastic products are thrown away indiscriminately, it will destroy the land environment and cause serious pollution. Therefore, for plastic products, domestic and foreign have always maintained the "plastic control" attitude. Plastic management has long been an important initiative in the global promotion of sustainable development process.

As early as January 1 this year, in order to manage plastic products, the EU has begun to impose a "plastic packaging tax". The specific measures are: disposable plastic packaging at a rate of 0.8 euros per kilogram tax.

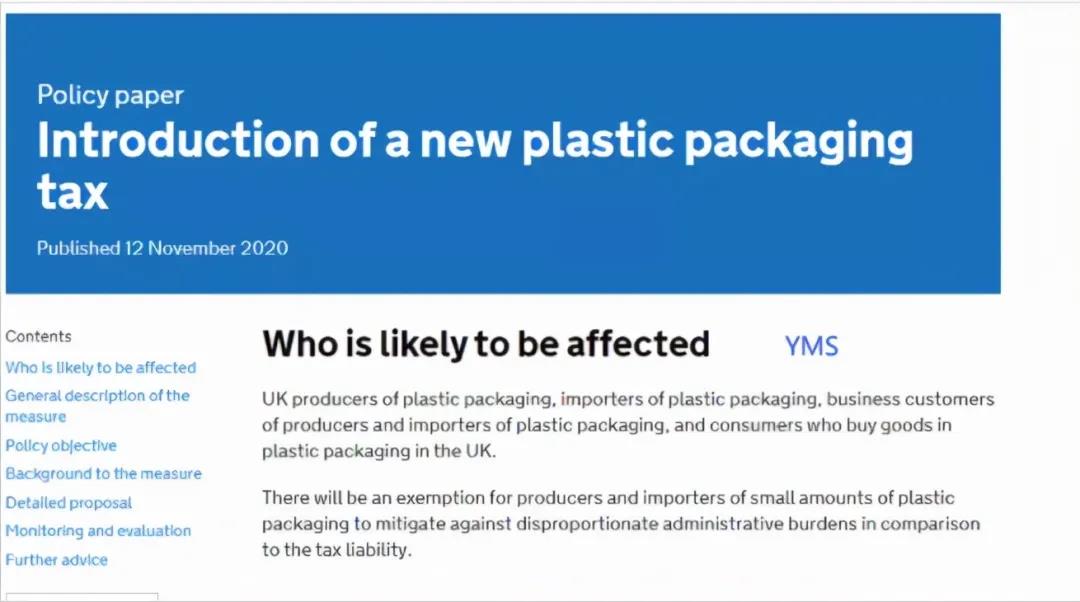

In addition to the EU, HM Revenue & Customs also issued a new tax last November, the Plastic Packaging Tax (PPT), which applies to plastic packaging produced in the UK or imported into the UK. It has been legislated in the Finance Bill 2021 and will take effect from April 1, 2022.

On plastic packaging tax, the General Administration of Customs said:The plastic packaging tax is to improve the level of recycling and collection of plastic waste, but also to urge importers to control the plastic products.

According to the resolution, manufacturers of plastic packaging in the UK, importers of plastic packaging, commercial customers of plastic packaging manufacturers and importers, and consumers who purchase plastic packaging goods in the UK are obliged to pay. However a small number of producers and importers of plastic packaging will receive tax exemptions to reduce the administrative burden that is disproportionate compared to the amount of tax payable.

The main elements of the plastic packaging tax:

1. a duty rate of £200 per tonne for less than 30% of recycled plastic packaging.

2. an exemption for businesses that produce and/or import less than 10 tonnes of plastic packaging in a 12-month period.

3. the scope of the tax by defining the type of taxable product and what can be recycled.

4. exemptions for producers and importers of small quantities of plastic packaging.

5. who is liable for the tax and needs to be registered with HMRC.

6. how the tax will be collected, recovered and enforced. ;

The tax will not be charged on plastic packaging that

1. have a recycled plastic content of 30% or more.

2. are made from a variety of materials where the plastic is not the heaviest by weight.

3. produced or imported for the direct packaging of licensed human drugs.

4. used as transport packaging to import products into the UK.

5. exported, filled or unfilled, unless it is used as a transport packaging to export the product to the UK.

Manufacturers or importers of the above plastic packaging, and businesses liable to pay this plastic packaging tax, should include a statement in their invoices stating that the tax has been paid. The invoicing rules were due to come into force in April 2022, but HMRC has recently said it plans to delay them and that specific requirements and information will be published as soon as possible to give businesses time to prepare accordingly.